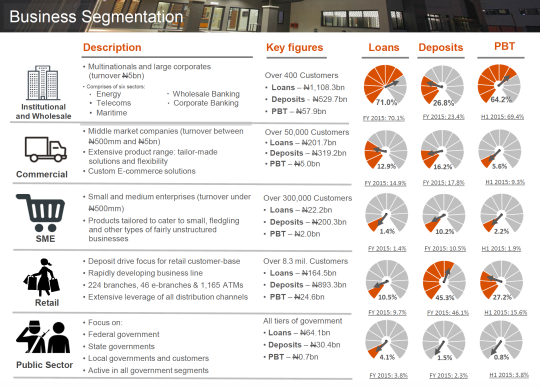

But something else caught my attention. This image from GTB report

As you can see, retail account for the largest deposit at 45% while they accessed less than 11% loan. Similar ratio applies for SMEs. Whereas, the only “groups” that got more loans than deposits ratios are public sector and institutions.

It’s also obvious that Banks earn their highest PBT from this institutional players.

We can easily see why access to capital is one of the reasons local businesses die. Banks are not our friends.

however, considering a number of other factors, its just Pareto at play here. I’m sure they’d love to support the retail and SME end of things. The operational landscape just makes it difficult

The report reveals why Nigerian banks are pretty much underperformers in their contribution to Nigerian economic growth. The critical sector which is SME is critically under-financed. They actually deposit almost 8 times more in GTB than they receive in loans. But why are they ignored? Apart from ridiculous interesst rates, most banks like GTB do not want to do the legwork and engage the SME. Its easier sitting in an air-conditioned office on a highstreet and doing 1 deal of 250 million at a go for some large corporate than 100 2.5 million deals with SMEs.

Indeed one only has to look at all the SME areas that are booming in Nigeria. In Nigeria, private hospitals are built without decent architectural design and ancient bedding due to lack of long-term lending facilities. In Nigeria, private office or residential buildings are built with poor water, sewage and electrical systems. In Nigeria, private schools are built with poor furniture and fittings. In Nigeria retail wholesalers do business from primitive plazas and clustered shops. In Nigeria, university hostels are built with inadequate toilets, kitchen facilities and recreational space. Yet all these businesses are profitable within a 5-10 year period. A little lending in all these areas would go a long way in boosting GDP because a 20 bed hospital could easily with lending be a 50 bed hospital with lots more staff and modern equipment.

Meanwhile the product of a misallocation of capital can be seen in real estate where skyscrapers built in Lagos for a high end corporate client lack customers or shopping malls built by expensive contractors lack sufficient well-heeled tenants, or “luxury” residences which again will be priced out of the reach of the middle class. Worse for many banks they were lending to the boys club of fuel importers, government contractors and power sector crooks.

I tried to make the assumption that all depositors also got a loan, that means that

400 institutional players yielded N57billion

300,000 SMEs yielded N2billion

But then you realise that the ratio of the loans is almost 50X in favour of the BIG guys (N1,108.3b : N22.2b) whereas, the value to the bank (PBT) is only 29X (N57.9b : N2b). That is merely like half the return compared to when they give the money to SMEs.

The question for me is that what is the motivation for Banks who prefer NOT to fund SMEs despite the fact that they might make more from that market? I know the number of deals needed maybe more and as @blacquay noted… [quote=“blacquay, post:2, topic:9427”]

…The operational landscape just makes it difficult

[/quote]

I believe there is an opportunity for collaboration that can be tapped in this gap. Who knows any startup doing this or planning to work in this space?

Thats not how bankers perceive it. They look at size as an indicator of risk. This is why over 30/billion dollars of loans made to so called large players are non performing.

Nigerian bankers don’t understand SME finance otherwise if they spent time they would unearth gold. There are a lot of pharmacies in Nigeria that do 5-10 million in sales that don’t have something as basic as a Cash register. In the western world banks finance this. There was a singlw location mama Calabar restaurant in Lagos I used to eat at that does over 300,000 a day in sales. Great food but basic plastic furniture and decor that could have been upgraded with the help of a loan. I bet lots of bankers ate at that joint before running off to offer Sweet Sensation and Tetrazzini loans.

I have absolutely no respect for Nigerian bankers. They are generally a lazy and oftentimes crookish lot.

We are actually in our own way working with SMEs in Nigeria. Its has been a long journey because trying to convince most SMEs to pay has been an issue.

We are now offering our core HR software free, with other packages a small fee. Just as from the bank perspective its difficult to find these SMEs and scale quickly. I do feel that more SMEs in Nigeria also need value added services just as HR & accounting to be truly ready for loans.

It would be interesting to learn more about how to work hand in hand with SMEs the data seems to be scattered.

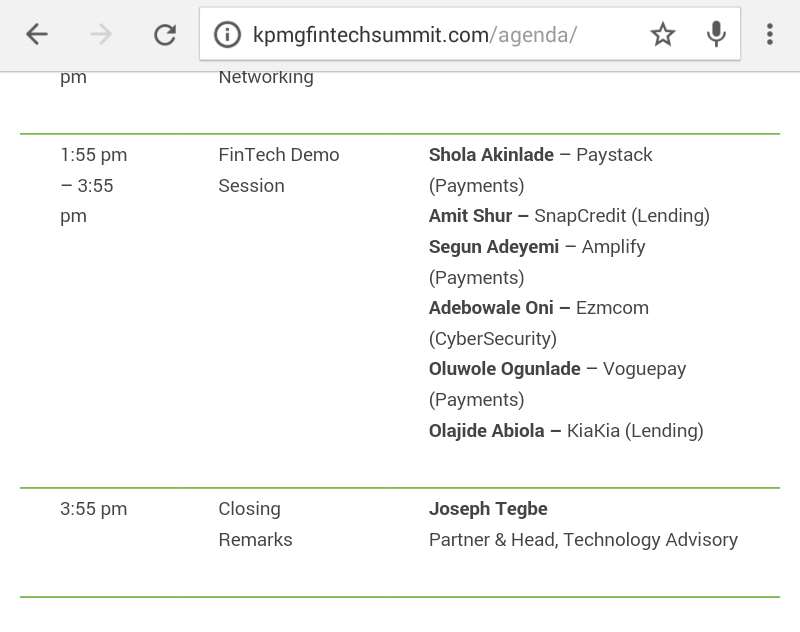

There are some excellent thoughts on how this issue can be solved from this @PapaOlabode’s article. It is a starting point of how to look at the solution to the REAL problems.

As he noted, I believe KPMG fintech summit is an interesting move that can facilitate fintech adoption for legacy institutions. For me It was an awesome event to attend (and be privileged to speak at)

This I agree with. And I think that’s the point a lot of startups (like myself), need to understand even while approaching the banks.

Yes, it’s tempting to work with banks. They’ve got customers - but there’s a lot of collaboration we can with other startups. That’s pretty much the summary of my take.

@spokentwice yeah I heard the conference was well attended. Any key highlights? Or if anyone has written a recap - pls shoot it my way. Thx

What made the event interesting for me is that KPMG is a “trusted” institution that can engage both sides of the table.

The event generally was cool, it was streamed live to YouTube. All videos here.

The icing on the cake was that they invited some fintech players to pitch at the event.

Nigerian SMEs are ready for loans now the problem is Nigerian bankers are too stupid to see it. They are too busy peddling deposit accounts and that stupidity is why most of our SMEs lack the finance to scale in the sense of them hiring new people, upgrading their decor and furniture, opening new locations, becoming more efficient. Because they remain small individually owned and managed outfits with the vast majority having less than 5 employees that is a big reason why the market for talentbase is tiny and why you should not focus solely on Nigeria but expand globally until Nigeria fits your market profile.

Yeah actually making plans to expand outside of Nigeria. But we actually have a lot of SMEs that are just 5 employees that request for our software so it is much bigger than you think.

Nigerian bankers are lazy and don’t know a potential goldmine even when it’s staring them in the face. I personally know a friend who had a wonderful idea that even when I heard it, I was impressed. Went to meet the banks to fund it, no one budged after all it was not oil and gas related.

Depressing graph, but not surprising at all. Big banks are known to give out most of their loans to big companies, so I don’t see the essence of SMEs & retail banking with them.

Why do Nigerian SMEs not use microfinance banks more? Methinks this is an opportunity for smaller banks to cater to businesses that big banks are obviously ignoring.

@philiprohv, I know you are a banker, so can I put you on the spot?

What are the operational landscape issues

How do you think the operational landscape issues can be dealt with at scale (remember we are talking 24million SMEs here) I am particular about possible collaborations - between financial institutions and startups - that can bridge the gap

Operational landscape issues will include regulatory, infrastructural, social and shareholders’ interest.

Statistically speaking the 24 million SMEs do not even qualify to be called SME going by conventional banking and world bank definitions. NBS and even SMEDAN etc say there are 17M as at 2015 with 32.7M employees.

Let’s do a bit of compensation and say only 1% qualify to be in the SME bracket. That’s a whopping 170,000k small business.

You also need to do segmenting and sectoral analysis.

At the end of the day, here’s what the banks find:

The hassle is too much

Lack of indepth knowledge of business

Shortage of specialists in the banking sector who understand these guys.

High unprofessionalism and ethics amongst the SMEs.

+++ a host of other reasons.

Banks don’t do guts but risk based lending in Nigeria where even existence is a risk.

There are many reasons why banks should support SMEs. Least of all growth engineering. But it is what it is.

All the reasons you listed are not enough. This is why @Nwabu says Nigerian bankers are lazy. The banks have the resources to get a lot of these things done, but they will rather make easy money.

Let’s take the issue of bookkeeping a lot of SMEs have, what stops the bank from partnering with a firm who will sign up these businesses, put their books in order and automate their accounting by selling them software and have all these paid for from the loan.

I agree with you. It looks like the ideal direction for banks but they still do not play big in that space. I guess it could be because of the risk level of SME’s. Banks give out these loans to the big guys based on their potential to succeed and available collateral.I am guessing there is a greater level of risk to be taken in the case of SME’s.

Also, the CBN has made banking so competitive that no one wants to be the first to venture into that area and lose because of the potential consequence on their business and the CBN impact. I think the support to SME’s may have to come from some CBN directive of some sort.

That said, Flex Advance by One Finance is a start up that targets SMEs who have been unable to access traditional finance (from banks or MFIs) and provides them short term funds. They actually make paybacks easy for the SMEs.