In 2015, I got petty and walked into a Firstbank branch and immediately requested them to disable my SMS notification.

Reason? Well, N4/SMS from over a million account holders daily was outrageously an extreme money making scheme for the banks. I was okay with just notifications sent via email. ![]()

Interestingly, I received email notifications for a while and then it stopped. Again, I walked into a branch and inquired why my email notifications weren’t coming through and I was told I opted-out from receiving alerts. I was amazed they could go that far to trick me into re-activating my SMS alerts. I walked out and ever since, I literally log into my online or mobile bank to always check the status of a transaction.

Picture this! If you feel SMS is a sure alternative in case a person is out of data, I reckon there are occasion when those SMS come hours or a day later yeah.

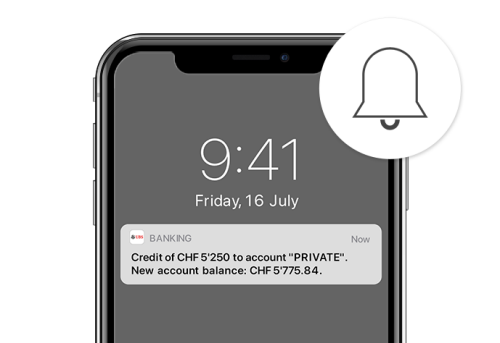

Fast forward to recent observations, the banks are just being petty for not enabling us to opt in for Push notifications – hence, messages that’ll pop up as alerts (especially credit alerts) on our mobile device.

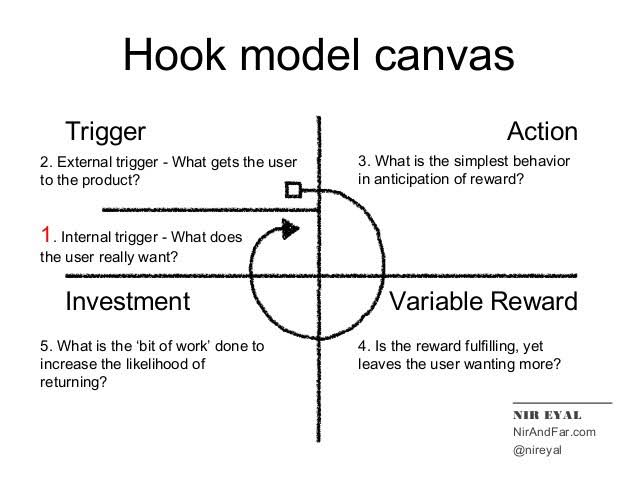

Banks can leverage push notifications to communicate with customers effectively. A lot of lesson can be learnt from the way that other industries are using them.

Recent years have seen a huge increase in customer expectations when it comes to mobile banking. From mobile alerts to apps and chat bots, there’s been a proliferation in terms of available communication channels. I personally would prefer a push notification to an SMS.

What’s more, I bet end users no longer want to be addressed en masse. Best results can be achieved when communications are tailored to individual circumstances at specific times. And remember, bespoke (credit) alerts will never be confused as sales messages or, worse still, spam.

Many banks have heavily invested in their apps over recent years, as a way of offering a digitally-savvy consumer base a more convenient way to access their accounts, so what’s the hold up with Push Notifications?

I want to believe I am not the only one who feels my bank should avail me the option to opt in for push notifications.

PS. I maintain personal and business accounts with Firstbank, UBA, Access Bank and Sterling Bank. None offers Push Notification.

What do you guys think?

.

.