Like a chart-topping song, “Cashless Economy” is a phrase that has enjoyed near endless ‘Mouth’ play in the Nigerian space in recent years.

Of course, some meaningful attempts at creating solutions in that space have been seen from both the private and public sectors.

However, with low adoption and impact, Nigeria still falls miles behind compared to contemporaries like Kenya (All hailmPesathe great) .

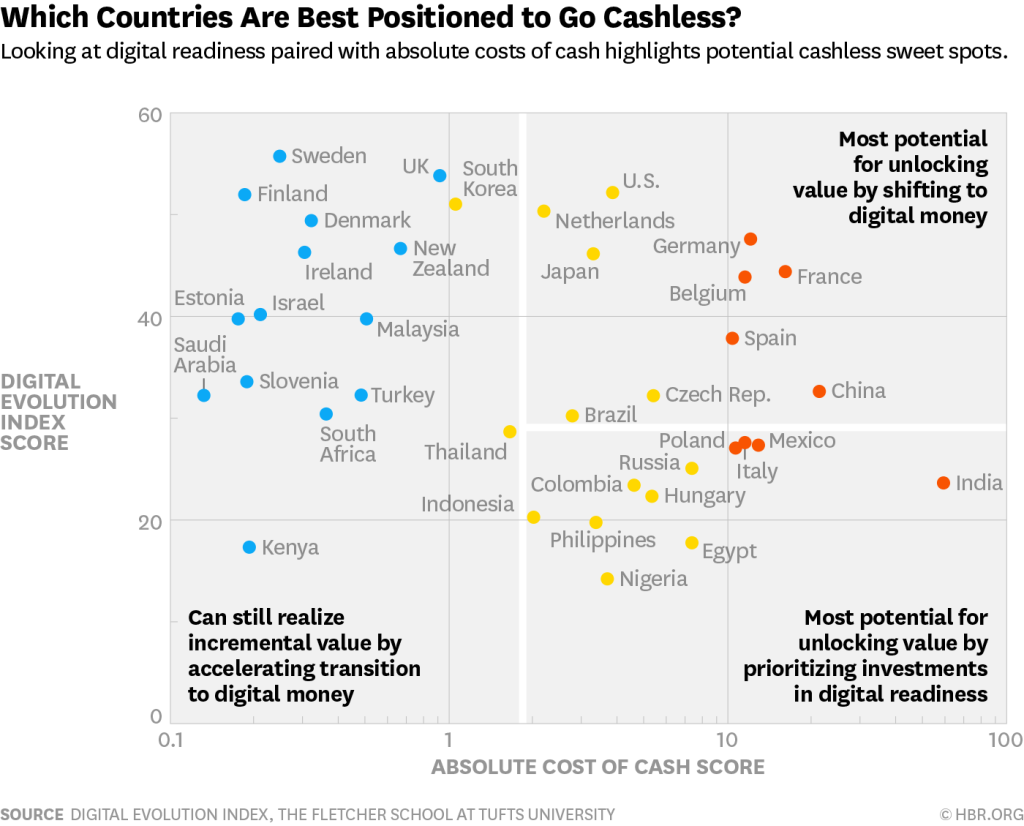

So, I stumbled today on this HBR article titled “The Countries That Would Profit Most from a Cashless World”, and I got stirred to the point of doing this - sharing with Y’all.

While not exactly new or surprising, the paragraph below caught my attention and had me think again of Nigeria’s lack of readiness for what lies just ahead;

…there are signs that cash is following the path of other “information goods,” such as printed photographs, cassette tapes, and DVDs in being replaced by digital alternatives.

From the analysis in the article (and from our everyday realities), it is obvious the cost of running a cash-based economy alone is sufficient a reason for us to push more pragmatically for a (more) cashless society.

Lately, seeing efforts that have been made in the mobile money space locally, I keep wondering why adoption is so low…and then I try to remind myself of the last time I ventured to use my Mobile Money service with _ _ _ _ - endpoint >> No conclusive answers ( Despite the fact that we’ve tried to use our “Paranoid Culture” as an excuse).

So, when I got to the point in this article where the question below is asked, I couldn’t disagree with the answers for the category Nigeria falls to.

So these are the questions I pose to this community;

What can be done by the private sector (Corporation, Investors, Innovators etc…) to catalyze digital readiness for a cashless world in order to grow adoption? (Yes, I couldn’t muster the courage to mention Government… )

How do we digitally evolve as a nation to the point of being capable to successfully migrate to digital alternatives to cash?

PS: It’d be great to hear from folks already playing in the FinTech domain.

We keep talking about cash as the problem when it is a symptom. There is a reason why value chains prefer cash to going cashless and that is the transaction cost of going cashless. A friend traded 1 Billion Naira of Airtime and decided to use the banks, he ended up with a 4 Million Naira loss because of charges. I actually simulated it and got the same results. He traded in cash and made a profit. That there is a no-brainer.

In that post, I suggested a new hypothesis we can test based on my observations.

You can’t beat cash where it is strongest. It is a waste of time. You have to be like cash to beat cash. Nothing offers less friction and lower transaction cost at the transaction interface in Africa than cash.

People can do PhDs on this subject and nothing will happen unless we start testing out new models on the ground. Unfortunately, all the guys doing all the talking are not on the ground but in ivory towers like Tufts.

Transaction costs is indeed a big stumbling block. But it’s fair to say that not everyone is transacting at the N1billion Naira volume. However friction is where I feel it really breaks down. Right now in the bid to ‘capture the market’, the main players unknowingly introducing more friction into the system. So below 2 things happen:

Multiple products competing for attention or purporting to do one new thing or the other. Like seriously how many mobile money, wallet, new way of paying your bills, buying airtime etc do we have now?

The multiple products rarely work with each other. So if you walk into restaurant, you might ask ‘do you collect (insert latest mobile money)?’, before you start eating that poundo yam. A question you wouldn’t have to ask with cash. That’s why I agree with you that a product has to be like cash to beat cash.

Cash is simple. It’s ubiquitous with zero ambiguity of acceptance. That’s what a product needs to do eventually do. And it all starts by removing friction not transaction costs.

But friction might seem like an easy word to solve for but it’s actually complicated. How do you remove friction so you can use a product, the way you can use cash? A few factors to contend with are limitations by: regulatory hurdles (CBN/NIBSS limits), insufficient data (KYC is a joke), weak institutions (bankruptcy, civil court judgements for defaulters) etc. before even considering platform limitations or dependency on other aggregators.

Also sometimes folks over think the innovation angle as well. A real life example from the UK below shows how the common Visa/MasterCard card is eliminating cash:

Visa/MasterCard debit card or cash > purchase travel card or oyster > tap at barriers to travel on train/underground tube

Remove friction

Visa/MasterCard debit card > now tap directly at barriers to travel on train/underground tube

That’s how to think of the whole business of removing friction.

Aggregate transaction cost in a value chain matters as there would be no need for those at the top to initiate if the cost of running things become prohibitive. Nobody buys 1 Billion Naira airtime to use, but rather to sell through channels to the consumer.

While the consumer pays cash, the value chain bears the rest of the transaction cost in fees and that is worse than friction as it means models would cease to exist.

Models do exist outside traditional banking and formal or regulator approved electronic transaction models. They choose cash as the acceptance protocol because of transaction cost. If it made sense to them to use existing mechanisms to trade, they would have and they would also change buyer behavior with acceptance.

The consumer is overrated when it comes to transactions, we fail to realize that the merchant actually decides acceptance. Oyster is better than cash for British Underground and it also helps the consumer. The consumer didn’t choose Oyster really, it was an option provided at first, now it is mandatory to use contactless cards. Even for buses. London transport eliminated cash because of the costs to them.

In a competitive environment where people really know what they are doing, providers would court merchants and make them their “change agents”. I think I actually wrote something on that too a while back. I will search for it and post it here.

4 years ago before I lost completely all interest in fintech, and around the time when the initial set of mobile money licenses were being issued to Paga et al, my usual skepticism about their fate had led me to ponder the question “How do you replace cash?”. It dawned on me then that the solution that will win needed to scale effortlessly across all socioeconomic groups in Nigeria and therefore must at least provide the key qualities of cash that make it ubiquitous namely:

It must be fungible i.e. I must be able to exchange the credit for value immediately afterwards with anybody. Think “If I collect a credit from you, I should be able to use it to buy chewing gum a minute later”

It must obey the 10 second rule i.e. I should be able to conclude a transaction in 10 seconds. Think “how long does it take to pay an okada man or how long does it take a conductor to collect his cash from each passenger and give change”

It must enable micro transactions. Majority of cash transactions are micro transactions. Danfo N100. Gala N50. Airtime N200 etc. This means transaction costs must be eliminated or kept to a single digit maximum. Preferably the former in keeping with how cash works.

The U.K. Oyster system complies with (2) and (3) which explains why it is widely used but still a closed loop system. To enable the general case, the winning solution must also meet (1).

I actually came up with a unique solution but alas due to the “Nigerian Factor”, I’ve lost all interest.

Really good write up. Below quote (emphasis mine) is from your post and strangely summarises the point I was making about friction.

In any case, let’s even examine the oyster usage again. Of course you’re right that this was imposed by the TFL. However, the rise of the usage of contactless is not imposed by TFL but instead driven by consumer behaviour. BTW, there are a lot of stories about people bumping into strangers with devices, to fraudulently obtain money from the contactless cards. Why do people still use them? Because they know they won’t go out of pocket and there’s recourse to either their bank or insurer.

Maybe you’re right that transaction costs is the greater hurdle. However, what you’ve described suggests an incumbent status or regulatory power to provide one solution to rule-them-all. I don’t agree with that approach. Matter of fact, UK is gradually becoming a cashless society due to a myriad of factors which appears to me that they’re solving to reduce friction.

)

)