Kept scrolling to find the Nigerian. Much disappointed.

3 Likes

Same sentiment too, when I first read about this. I kept reading hoping to find a Nigerian name . I mentioned @asemota in the conversation sef, I just weak.

1 Like

We were busy whining and crying away…

Someone else saw an opportunity where we couldn’t see beyond the problems.

NIGERIA!

Very CX-centric Model. Captures major concerns of target market e.g User Privacy, Transparency.

1 Like

Didn’t Diamond Bank launch a similar app, but a closed loop version recently? - eSUSU

I am also aware of a few others out there, but may never go mainstream cos they have all failed to address the very pain point (members default) associated with SUSU schemes. They have simply digitized the experience not solve a problem.

See why bank-led innovations hardly win? Getting people to adopt electronic ‘SUSU’ is hard enough, then you have to layer the internet banking and token gateman there.

Why not just create a super-dumb product on web and mobile, open up debit channels to self deposits, card-on-file, airtime, direct debit…, and open up disbursements to any bank, and enjoy the benefits of being the funds intermediary/escrow/administrator?

When the crux of every initiative = either more bank accounts/more prepaid cards/more bank mobile wallet/more app downloads/more payments through my gateway…, it means they don’t really get the point yet.

I watched the how-to video. I understood it, but only because I listened enough to write this comment.

4 Likes

There’s also a Sarah Bullock, so I’m not particularly motivated to go on that goose chase.

3 Likes

Nigerian banks are still learning to be agnostic and Access Bank is leading in that area. Let’s give them some time, they will eventually jettison their walled garden approach.

1 Like

I agree with this. My little knowledge of why this breaks down is because providers always seem to think of themselves (create a new platform or product e.g mobile money, QR/NFC payments), rather than the customers (who just want to pay or get paid). As if customers wake up and say which new technology should I adopt today.

No one seems to think collaboration (for the benefit of the customers) rather than competition (to own ‘market’). Which is super weird especially as fintech by its nature is fragmented and require services to be aggregated from other players, to provide end-to-end service.

In terms of e-susu itself, it’s of course an hackaton effort, so expected to be far from finished. But it does a good job in telling the story of solving a genuine need. However it’s aimed to be a consumer fintech app, therefore regulatory hurdles will mean that it can only tackle a region at a time. For example, if it has to launch in US,U.K. and France, then will likely encounter SEC, PRA and ACPR respectively. Taking money off friends & family doesn’t mean there’s no credit & default risk. At the moment, it’s just a dashboard that can be replicated. Quite easily for the next hackaton.

2 Likes

What is interesting about this type of appropriation is that nobody will sue them for trademark infringement. Not even one person from Africa where it is was adopted from and people have even used it as their registered company names. Meanwhile, I registered a domain once and I got a letter from a trademark owner in America. They said the name was too close to their trademark. I told them to fuck off but I forgot that I registered it using a US credit card and address. Heck! We even had a bank called Susu Micro Finance bank that was run by a former classmate Toyin. Maybe I should contact her and tell these chaps to get a lawyered up.

That is another conversation entirely and I blame the regulators 100%. Try launch something like this in Nigeria and the next thing you will hear is CBN knocking.

7 Likes

Recently, I learnt if you use the word “wallet” in your service, it means you want to have CBN hitting you.

1 Like

Its like asking to be regulated as a bank.

I knew I’d heard of something similar to this e-susu ,its actually the Susu Microfinance Bank you mentioned.

I strongly remember being at a local event at either CCHub or iDEA where a team pitched an app like this. Not sure what happened to them.

i saw that name and the profile pic, it rang a bell too

Two Nigerians are a member of the team behind the Esusu app,just not public members.

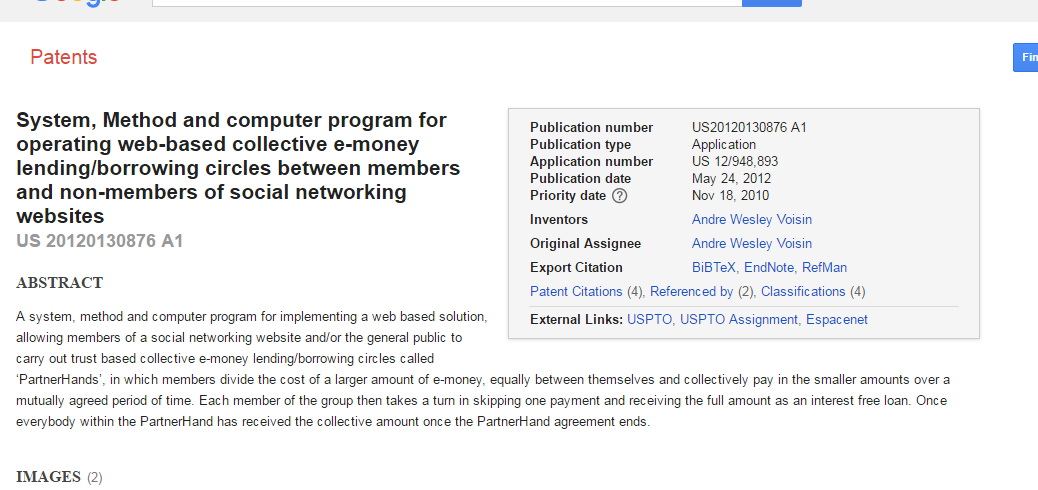

That’s a US patent. How are they exploiting you?

I think they are doing something similar in Kenya for SACCOS: https://www.homepesasacco.com/index.php and http://www.kachwanya.com/2016/06/20/homepesa-sacco-limited/?utm_content=buffer0e316

And, Airtel Weza in Uganda: http://www.grameenfoundation.org/introducing-airtel-weza-uganda

I may be totally off the wall thinking this way but given how popular savings groups are in certain African countries and their growing traction in various diasporas, this could be an interesting opportunity for another Africa-based startup to develop such products with international appeal - assuming it could get some financing. Or, this thought is just the uniformed ramblings of your resident Oyibo.

6 Likes